How is the new standard IFRS15 affecting companies?

This standard relies on the concept of transfer of control to recognise revenue, rather than on risks and rewards as previously. It requires a contract to be broken down into distinct performance obligations, each with their own margin and pattern of revenue recognition.

Could IFRS 15 therefore call into question the recognition of revenue according to the stage of completion, or lead to a change in the pattern at which revenue and/or the margin is recognised?

In the attached document we have analyzed the impact of IFRS 15 from a sample of 73 European groups.

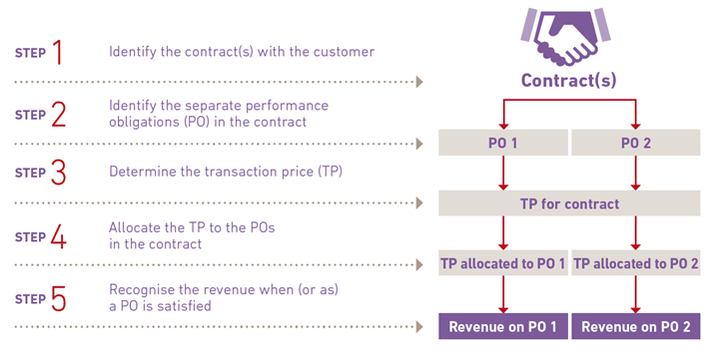

Next we analyzed the 5-step recognition model established by IFRS 15.

Contact