Want to know more?

Both large multinationals and small and medium enterprises have been forced to dry up their production, leaving thousands of jobs up in the air. A slowdown in household consumption may stop growth prospects if appropriate measures are not taken.

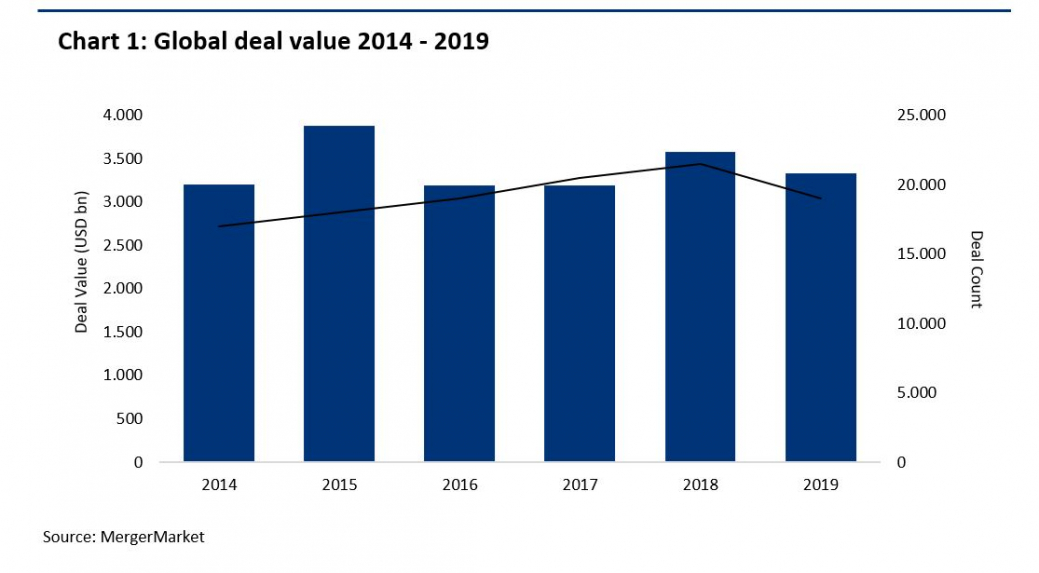

This situation will affect the M&A market, but not in a linear way. After an exceptional 2018, Global Corporate Finance deals have taken a slight dip in 2019 and decreased about a 6.9%(1) but expectations for 2020 were positive and a strong movement was expected in the market. However, the arrival of COVID-19 casts some doubts on those prospects. Thus, it is interesting to understand what the main factors are that can make the positive trend in the world of M&A continue.

For the improvement of the circumstances generated, it is vital that the measures provided by both Governments and Central Banks help regenerate the economies, which are going to stand still for some weeks. The initiatives adopted must be consistent enough so that companies, beyond suffering the setback, do not drown. This includes temporary tax reductions, public and private financing, deferral of payments and assistance to maintain employees once the whole problem is over. Whatever the policies are, in our view, the intrinsic factors that drive the M&A industry will ensure that market activity is not overly constrained. The trend in corporate operations will be marked by two types of incentives:

Business incentives:

Over the next 10 years, the number of transactions between companies will rise because owners will be of retirement age. According to the National Association of Corporate Directors(2), fewer than a quarter of businessmen have a clear succession plan for their business. In addition, in times of uncertainty, conflicts of misalignment of interests flourish among partners, who are faced with different perspectives on how to deal with the situation. In those cases, an equity transaction (increase in capital by a new investor, sale to a third party, sale between partners, LBO, MBO, etc.) could be the perfect option for the shareholders.

Furthermore, the challenges in the medium term in some sectors such as medicine or retail, which will be highly focused on a more personalized and digital attention, will make small and medium enterprises choose to continue their business by integrating into bigger companies. These industries will be preferred targets for acquisitions: given their importance during the current situation of social isolation, as well as their general growth trend, they are a clear option for PE Funds or for international competitors.

On the other hand, COVID-19's crisis management is showing many shareholders that any unexpected event can eliminate their expected returns. In an industry study carried out by Mazars, we can see that the effects of this crisis may be very different depending on the sector. Retail, leisure, travel or industry will suffer significant falls in their activity in the short term, so they will have to resort to advice on business restructuring, search for financing or access to regional, state and European aid. However, industries like health, food or companies with a high level of digitization will maintain their operating accounts more successfully, so they will take advantage of the situation and will invest in companies in their market to gain share and access new markets, taking advantage of synergies.

Investment incentives:

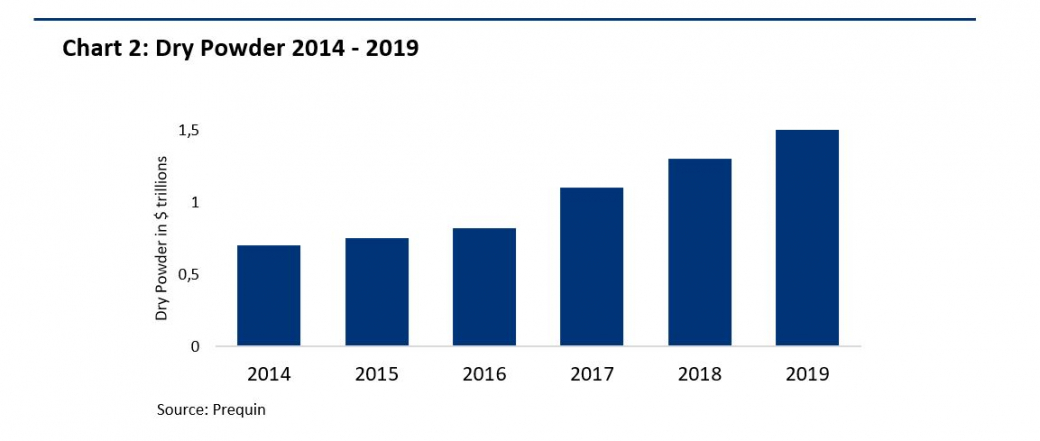

Private equity firms have started the year 2020 with a record level of cash, amounting to $1,5 Trillion(3), and are willing to invest it. The current market situation makes investment funds with high liquidity available for investment focus their objectives on different investments rather than the traditional buyout. Sectors such as travel, restaurants or hotels, with a consolidated business model but liquidity problems due to this crisis are more likely to be invested in by a PE. In any case, during the next few months a high level of activity is expected from funds trying to invest the available cash.

As we can see relating charts 1 and 2, during the last years the dry powder available has been about one third of the total deal value of the year. However, at the end of 2019, the $1.5 trillion mean a 50% of the total deal value of the year. This fact could lead to an increase in the M&A market up to $4 trillion, a record only achieved in 2015. Additionally, the central banks will maintain low interest rates in order to help economies recover the previous GDP and growth levels.

The amount of money of venture capital, the improvements in certain companies and industries after the crisis, and the liquidity pumped by central banks at low rates form the perfect storm to boost acquisitions, whether by funds or other companies.

In short, we can say that there are some reasons for optimism. In order to successfully close corporate deals, especially in the current difficult situation, companies must be very well prepared. Stakeholders must be able to form a team with a multidisciplinary approach that considers the different fiscal, financial, commercial or market aspects that will be relevant after overcoming the COVID-19.

The Coronavirus is having serious impact on the health of hundreds of thousands of people worldwide,

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.